In June 2018, the Fantasy Sports Trade Association (FSTA) released its annual market research findings conducted by IPSOS. This year’s report had a key aim: to discover any overlaps in participation behaviour between fantasy sports and sports betting, and to determine the potential effects on both industries.

The report found that of the 980 fantasy players and 979 sports bettors surveyed, an identical percentage (51.5%) of each group played each product exclusively, with 475 (or 32%) of those surveyed across both categories crossing over, having participated in both fantasy sports (DFS and/or traditional leagues) and sports betting in the past year.

JOAKIM RENMAN is Scout Gaming’s commercial director and has spent 11 years in the igaming industry. Joakim has worked with most of the biggest operators and suppliers in the industry and is responsible for the Scout Gaming’s commercial strategy.

One particularly interesting fact was that DFS players play more frequently than sports bettors, with 73% participating at least on a weekly basis.

Just 59% of sports bettors said they took part weekly. Among crossover players, the participation frequency increases significantly with 80% of playing DFS on a weekly basis, and 70% placing sports bets on a weekly basis.

Meanwhile, crossover players are 20% more likely than exclusive sports bettors to engage in wagering on a weekly basis, making a strong case for operators to try to marry the two concepts. Crossover players also spend more across the board.

Perhaps unsurprisingly, crossover players are also more likely to make parlay bets. After all, the practice of combining selections into a single bet requires the exact same pre-match analysis as when building a fantasy team. Combination bets were placed by 82% of crossover players, compared to 65% of exclusive sports bettors.

On an associated note, fears that sports betting will cannibalise fantasy play appear to be completely unfounded, with 86% of traditional sports bettors and 78% of DFS players expecting to play just as often following the PASPA ruling.

Other findings from the report showed that fantasy players, and in particular DFS players, tend to have higher access to digital devices, signalling a higher marketability towards the fantasy population. The general trend in Europe is that big-spending players tend to use mobile devices, with 60% favouring them over desktop machines. DFS players also rank highest in all categories of data and premium advice services, spending more to help improve their play.

Key takeaways:

• Nearly half of the current sports betting population in the US also play fantasy sports (and vice versa)

• Compared to traditional fantasy, DFS has a high degree of crossover with sports betting, and is likely to be the “point of entry” for sports bettors.

• Crossover players are heavily involved in all aspects of fantasy play and sports betting; they play more often, across a greater number of sports, and spend more on related services.

• Few fantasy players will lessen their fantasy sports involvement due to impending legalisation.

The US Supreme Court ruling earlier this year not only paved the way for each state to regulate sports betting but it also raised the hackles of the major sports leagues (NFL, NBA, MLB, NHL and NCAA) who have long opposed regulation on the grounds that making something easier to bet on would increase the risks of match-fixing.

In some circumstances this might be a valid argument, but not given what we know of the US, the leagues and our experiences of sports betting around the world.

Sports betting in the US is not a new thing. Nevada has offered sports betting for as long as anyone can remember. This, together with the number of offshore operators targeting the US and cryptocurrency sportsbooks trading under a us domain, illegal back-street bookies and references to betting in shows as diverse as Frasier and Murder, She Wrote, all suggest that sports betting is, and always has been, going on outside Nevada too.

While the leagues may have integrity concerns about sports betting proper, they appear to have been more relaxed in the case of daily fantasy sports, in which the leagues have vested interests but which Nevada and others decided is effectively sports betting by another name.

A lack of regulated betting does not prevent integrity issues: in 2007 an NBA referee was caught betting on games he officiated in. There have also been shenanigans relating to the New Orleans Saints ‘pay to injure’ scheme (2009-1 1), which offered players incentives to injure players of opposing teams and, more recently, the New England Patriots deflating footballs to make them easier to throw and catch. Then there is Brian Tuohy’s book ‘The Fix Is In’, alleging that the NFL is rigged.

If this alone were not enough, experience in other parts of the world suggests that far from increasing match-fixing, if the recommendation of the Law Commission in India is any indicator, regulated betting would be the best way of tackling integrity issues, bringing to light an activity which is best protected when done in the dark or at a distance with illegal or overseas operators.

As Jay Kornegay, VP of race and sports superbook at the Westgate Las Vegas Resort and Casino, put it recently: “People aren’t going to want to bet on something that they don’t think is fair and true.” Fact is, it could be argued that without regulated operators some of the subtler forms of match- and spot-fixing would never have come to light, in which case maybe the leagues should be paying the operators for doing their job for them.

Finally, the play and the players: the status and earnings that go with being a professional league player dwarfs anything a match-fixer could offer; this, together with the statistics, analysis and punditry (both of the professional and armchair variety) only further dilutes the leagues’ argument.

So, if not integrity then what? What is this really about? In explaining his league’s position, NBA commissioner Adam Silver said quite clearly: “We’ll spend roughly $7.5 billion dollars creating NBA basketball this season. And to the extent that product is then used for casinos, betting parlours to make money on, we feel, just in the same way a musician that receives a royalty for the music that’s being played, we should receive some sort of royalty. So, call it a royalty, call it an integrity fee, we will have additional expenses and it’s ultimately our intellectual property, and we think we should be compensated for it.”

As Mr Silver says, call it an “integrity fee”, or if it’s about intellectual property rights then a data fee, something which reared its head in West Virginia, where the NBA, MLB and the PGA Tour pushed for the mandatory use of league-supplied data (at a cost) and also wanted a say into the types of wagers allowed in the state, and which caused West Virginia Gaming and Racing Association president John Cavacini to declaim as “nothing new. It’s the same language. It’s a money grab by major league sports.”

This analysis of the league’s position appeared to be reiterated during a panel debate at G2E where MLB executive vice president Kenny Gersh suggested that the integrity fee should be called a ‘royalty’ and that leagues had already lowered their request to 0.25% of betting revenues from their starting point of 1%.

It seems that most legislators have seen through the integrity fee argument and rejected it. That does not mean that the fight is over, however. The leagues could get what they want in other ways, for example by changing where they hold events and favouring those states and stakeholders which support them. Remember that the NCAA allegedly persuaded Oregon to stop parlay sports betting in 2007 by prohibiting the state from hosting championship basketball games, following in the steps of the NBA, which did the same.

According to a number of estimates, the four major sports leagues are already going to benefit financially from regulated sports betting — from a modest $4.2 billion a year between them to an estimated $14.8 billion annually for the NFL alone — indirectly through increased fan engagement, TV advertising spend, sponsorship, merchandising and data and picture rights.

On top of this are the prospective (very lucrative) partnership deals such as the one between the NBA and MGM Resorts as its official betting/gaming partner, which in turn raises the issue of ‘poacher and gamekeeper’ and begs the question: just how much and exactly what action would the leagues be willing to take in the name of integrity, when that same action would have a direct impact on their own bottom lines?

All of this means only one thing: if the whole debate is about money, then the question becomes how far will the leagues go to secure the ‘compensation’ they feel is their due?

In this context the question of integrity is no longer about sports betting and match-fixing. It is one about the integrity of the sports leagues themselves.

Christina Thakor-Rankin is principal consultant at 1710 Gaming, working with start-up, evolving and established operators internationally, regulators and industry groups. Her work covers all aspects of the gaming and gambling cycle, from initial research, licence and operational go-live, to new markets and opportunities, consumer engagement and experience. Christina’s 20-plus years of industry experience includes management roles at William Hill, Blue Square, Tote (Sport) and Virgin Games.

iGaming Business: Can you give us some background to GoWild?

Itai Zak: GoWild launched in 2008 and has been on a steady growth path ever since. Today we operate several brands focused on a number of key markets, in particular the UK, the Nordic region and Germany. Originally a Microgaming casino, in early 2017 we embarked on a rather complicated migration to our own proprietary igaming platform, GoWild HERO. This platform is connected to more than 30 leading game providers, giving players access to more than 1,500 unique games.

Since we control it, this new platform also gives us much more flexibility to launch innovative concepts, offerings and campaigns faster than ever. We launched in the UK in November 2017 and our performance since then has exceeded all expectations, with the casino’s popularity spreading at an incredible pace through 2018. During this period, we also saw exceptional growth in our core markets, as well as overall improvements across all main KPIs.

All these developments across markets and technology have of course resulted in a larger team and we now have some 200 professionals supporting our many endeavours.

Which recent slot titles are performing particularly well for GoWild?

I’d say the NetEnt classics such as Starburst. Its Jumanjii slot game has also proven a hit, as has the Book of Dead game from Play’n GO. In the UK, several Scientific Gaming and Greentube titles are also performing well. But overall, the slot classics seem to work best.

Which supplier’s content performs most strongly and consistently for GoWild, and why?

We’re currently working with about 30 providers, but in general the bigger ones like NetEnt, Microgaming, Evolution, Scientific Gaming, Novomatic and others such as iSoftBet and Play’n GO tend to lead in terms of popularity and play.

In other words, it’s clear that different software providers and different games are preferred in different places. No one provider fits all markets, which means that even with 30 software providers powering our platform there is a market for everyone.

You take content from a number of suppliers. From your side, what would you like to see them do better or more of?

In all fairness, the software providers are constantly coming up with new games to attract customers. Usually these are classic games with a twist or new themes for games like slots. This is great for the marketing buzz, but I have to say the industry as a whole could use more innovation.

For example, we’d like to see more abilities and tools embedded in the games to better engage with players and interact with them in real-time. Ideally, the suppliers would have some kind of open API which would allow the operators to immediately interact with players based on specific trigger events – such as a big win or a big loss.

From our perspective, unique ways to interact and communicate with players in real-time is key to improving the content and thus enhancing the overall customer experience.

How do you decide the position of games on your homepage? Is it purely down to what players are staking on, or do you use other tools and techniques to make this more dynamic?

We have a dynamic system which analyses the performance of our entire games catalogue on a weekly and monthly basis according to a wide range of parameters. For example, the system considers things such as the popularity of the games, including aspects like how many bets were placed on the game and how many unique players played the game in any given timeframe.

This analysis is done per country and per player segment, in order to gain an even deeper picture of engagement and to personalise each player’s experience as much as possible.

Of course we also have specific algorithms regarding how to promote new games and how much exposure to give them. Bottom line, we’re using some seriously strong technology and stats to get the job done, both on the homepage and elsewhere.

What would you say are the major challenges for a CEO of a pureplay online casino in 2018?

The challenges I’ve faced in 2018 are basically the challenges that all online casinos face over time. This is a super-competitive space, which means we need to always be on top of our game, diversifying our business and entering new markets. This is particularly true as the challenges of regulation and strict compliance mount. We’ve grown a lot over the last three years and plan to continue growing. To do so we have a lot of ambitious plans in the works, especially in terms of product and UX.

To meet these challenges and expand, we need a dedicated team, which is a challenge in itself. It’s not always easy finding good people and retaining them. That’s why we invest a lot of effort in identifying and attracting the right employees, with proactive measures to encourage them to excel year-over-year.

What is your primary focus for the product side of the business over the next 12-18 months?

We’ll be expanding our footprint in our core markets in a number of ways. For starters, we’re in the process of creating a totally unprecedented marketing approach for our UK players that will eliminate the use of bonuses and promotions in the way that they’ve been used until now.

Beyond that, we’re continuing to put a huge amount of emphasis on personalisation tactics, so that we’re able to offer players as personal an experience as possible. While we’re certainly pioneering in that realm, we know there’s much more to do!

In terms of our overall business plans we’ll be concentrating on three areas: we’re going to be launching a new brand focused on the Nordic and German markets, and we’ll be looking at virtual games and sports betting to launch new product verticals. Finally, we plan to expand the GoWild brand into one new regulated market in 2019.

After spending many years in the gaming industry, both offline and online, as a team we were somewhat tired of seeing things not going how they should. Rather than sit and whine about it, though, we decided to make a change.

InPlayNet was set up to bring what we thought was needed to the gaming industry, to not only create for online but to develop something new for the online and offline industry, and tie the two worlds together. Taking the best people from the world of igaming with over 400 years of experience between them, a group of like-minded individuals became the InPlayNet team.

After three years of research and development, a lot of coffee, a few sleepless nights and lots of testing, the InPlayNet platform was created.

JOHN GREENACRE is CTO of InPlayNet Entertainment Limited. Coming from a technical background in the offline gambling industry, he has worked with some of the world’s leading online operators and providers.

What we do different

We built the whole platform based on three core principles: usability, stability and speed. We started building from the ground up, using the latest architectures available, which allows the platform to deliver content at speeds over 200x faster than some of our competitors. This speed was utilised in the back office as well as the front-end of our clients’ sites, thus benefiting both players and users.

Optimised for today’s market

Speed was not the only consideration. As the sports betting industry and players have changed over the years, so has the way in which players bet. No longer is it all desktop-orientated as more and more players switch to mobile devices as their primary option for betting. Our platform is fully optimized for all mobile devices. So, whether you are in front of a PC, looking at a tablet, or on the train betting from your mobile phone, the platform serves you the most optimised website.

Quantity and quality can co-exist

Although the InPlayNet platform is one of the fastest available, we didn’t want it to be all about speed. We built up our own bookmaker and risk management teams to ensure that the sports betting offering was second to none. With this we are able to offer more bets and more bonuses to our clients, which means their players are retained for the long-term. Offering “Add Game”, “Cash Out”, “Partial Cash Out”, “Free Bet”, “3+1”, “Change Game”, “Remove Game” and more, the InPlayNet sport offering exceeds all expectations for both operators and players alike.

Here for you

The platform isn’t built just for players; the back office is a real pleasure to work with also. With integrated CRM, bonus, affiliate, marketing and reporting systems included in the platform, it means that everything is in one place and all information is directly at your fingertips. InPlayNet also includes our own custom payment portal and game management system. The best performing platform is also backed by 24-hour support.

Into the future

We don’t intend to rest on our laurels and are adding live horse racing, dog racing and a full esport package to our offer. InPlayNet will be working with the best providers around the globe to bring the best content to their clients, now and forever.

COMPANY PROFILE

•NAME INPLAYNET ENTERTAINMENT LIMITED •FOUNDED 2017 •SECTOR ONLINE PLATFORM •WEBSITEINPLAYNET.COM

In the UK, much of the online casino market is driven by two key segments: sports betting and bingo.

But while sports and bingo sites are similar in that they both have casino pages offering slot content for their customer, they appeal to completely different segments of the gambling base.

This analysis will look at the difference in casino slot content between these two groups of sites.

We will also take a look at Playtech game content, unique in that this commands significant presence on operator sites through their exclusive sportsbook ‘casino’ tabs as well as through its Virtue Fusion platform which powers many bingo sites.

Sites analysed

The 10 bingo and 10 sports sites we compared are shown below.

We looked at the games in the top 10 positions of each page every day from 1 June to 30 September and aggregated the data to get the top 20 positions.

So how did we decide which sites to analyse? We simply typed ‘bingo’ for the top 10 ranking bingo sites and ‘football bet’ for the top 10 sports betting sites.

You will notice that many of the sports betting sites have multiple casino tabs, for example ‘Casino’, ‘Vegas’, ‘Arcade’ etc. We used all of them for this analysis. If a site had multiple tabs with slot content, each page was given equal weighting.

The following home pages were analysed: Crown Bingo (home), Foxy Bingo (home), Gala Bingo Games, Lucky Pants Bingo (home), Mecca Bingo (home), Mirror Bingo (home), Sky Bingo Games, Sun Bingo (home), William Hill Bingo (home) and Wink Bingo (home).

Sports betting sites analysed were Betbright Casino (home), Betbright Games (home), Betfair Arcade, Betfair Casino, Betvictor Featured Favourites, Betway Casino (home), Betway Vegas (home), Bwin Casino (home), Coral Casino Top Games, Ladbrokes Casino (home), Ladbrokes Games (home), Ladbrokes Slots (home), Paddy Power Casino (home), Paddy Power Games, Sky Casino, Sky Vegas Main, William Hill Casino, William Hill Games (home), William Hill Macau (home), William Hill Vegas (home).

Top ranking games

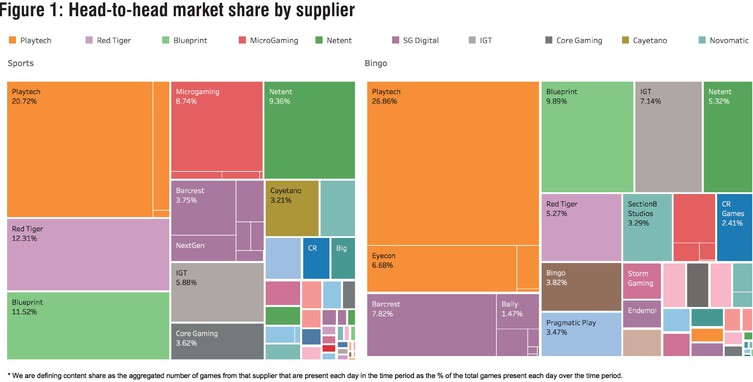

These show a significant difference in game content, although interestingly the same suppliers feature strongly in both sets of rankings.

There are also some similarities. SG Digital’s Rainbow Riches ranks number one for both sports betting and bingo sites, with Cleopatra (IGT) and Starburst (NetEnt) also in the top five for both.

We also see sports-related content such as Top Trumps World Football Stars and Frankie Dettori’s Magic 7 by Playtech ranking on sports betting sites.

Some providers also have markedly different content ranking across the two site groupings. Blueprint’s Pig Wizard for example is the highest-ranking title for bingo sites, though this slot title does not feature at all in the sports betting rankings.

The bingo rankings also feature TV show-branded content such as Love Island and Britain’s Got Talent. Aside from Deal or No Deal, TV-branded content does not feature in the top 20 for sports betting sites.

Playtech content

Playtech is unique in that its ownership of major bingo software supplier Virtue Fusion and exclusive ‘casino’ tabs on the major sportsbooks gives them significant market share for casino content across bingo and sports betting sites.

The acquisition of bingo slots-focused developer Eyecon and Quickspin reinforces their share across both segments.

Two of Playtech’s titles emphasise its focused content strategy. Fluffy Favourites by Eyecon has consistently been one of the most popular games on bingo sites since its release in 2016. Likewise, Frankie Dettori’s Magic 7 has consistently maintained a strong presence on sports betting sites.

Table 2 below shows the top-ranking games for both segments. On the sports pages Quickspin content is strongly present on tabs such as the ‘Coral slots’ page.

While Playtech has content on these ‘non-exclusive’ pages (which is increasing), the majority of their content is on tabs only containing Playtech games, such as ‘Bet365 Casino’ and ‘Sky Casino’.

Supplier content share

The heatmaps show the content share by suppliers for the tracked pages for September. It is important to note that it assumes that all pages tracked have equal weighting and it only considers the top 20 positions of each page.

For this, only slot content is considered; table games and live table games are omitted. (Playtech and NetEnt would have a higher share of these were considered).

Two other interesting insights arise from looking at the content. First, Red Tiger has significant presence on most of the slot pages of the major sports betting sites, as well as exclusive Macau tabs on two of the sites. So a relatively new company has made a big impact on the sports segment.

The second point is how the content share of Playtech in the bingo segment has increased with the acquisition of Eyecon, reinforcing their already dominant share through owning the Virtue Fusion network (see Figure 1).

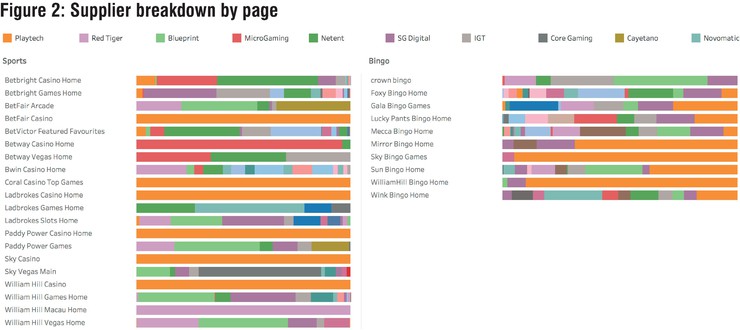

Page breakdown

Breaking down the content share further by looking at the supplier share on each casino page tracked, of the 10 bingo slots pages analysed, no less than nine feature Playtech/Eyecon content. On six of these, they command the largest share of content (see Figure 2).

This contrasts with the sports segment, where Playtech content is concentrated on its exclusive casino tabs.

Likewise, SG Digital has a presence on nine pages, though this is largely due to the success of the Rainbow Riches series.

Summing up

The type of slot content differs markedly across the bingo and sports segments. While the same suppliers are present, the content share differs. Playtech has the largest share of content on both the sports and bingo site groupings, with Eyecon content making a significant contribution to the bingo share.

iGaming Tracker – how it works

iGaming Tracker tracks hundreds of casino sites worldwide every day. From this data it can ascertain which games are on which sites and where they are positioned on the pages. It can also measure the market share of casino games suppliers by percentage of “real estate” on casino sites at any given date.

With more than 17 years’ experience in the gambling and sports industries, Ken Muir founded iGaming Tracker, which provides market intelligence services for the igaming industry, in 2015. Previously, he was at Perform Group as commercial director (direct to consumer sites) and Sky Betting & Gaming in various roles, including head of CRM and head of business strategy.

The scale of DDoS attacks has reached new orders of magnitude in the last year, both in terms of the power of individual events and the quantity that are taking place. While the igaming industry tends to suffer smaller attacks, most of which are conducted by disgruntled customers, of fundamental concern to operators will be that the sector attracts more attacks than any other area of business.

ROSS GAVEY is head of data centre sales at Sure International across the Channel Islands and Isle of Man. He works closely with clients across the gamut of Sure’s data centres and cloud services, DDoS protection and disaster recovery.

With attack capabilities entering the mainstream, US law enforcement has spent a good deal of 2018 focusing on taking ‘DDoS for hire’ services out of action. These services are becoming more easily available and as a result are putting DDoS capabilities in the hands of people with less technical expertise.

From an igaming perspective, these services enable a retail market in DDoS attacks to exist and they’re only likely to become more sophisticated as they learn from the larger, one-off attacks that are at the forefront of the threat environment.

Today’s exception is tomorrow’s norm

Security firm Corero corroborates content delivery network Akamai’s observation that most attacks are low-level. It reports that 95% of the attacks witnessed by its clients are 5Gbps or less, but that wasn’t the case this February when Github suffered an event measuring a record-breaking 1.3Tbps. Just a month later, a US-based ISP had to fend off a 1.7Tbps stream of data that was aimed squarely at knocking it offline.

The fact that DDoS is principally about disruption is likely to account for its popularity. In the main, attackers aren’t looking to steal credit card data or personal information. Their aim is to deny a service being used by its customers.

The damage is done in two ways. Firstly, they stop paying customers from using an online service, thus reducing revenues. Secondly, they can harm a brand to such an extent that once-loyal users consider heading elsewhere. In a 24/7/365 environment, service availability is crucial. By denying customers access to the igaming experience they want, attackers are counting on the fact that they’re hitting the sweet spot where dipping revenues and deserting customers collide.

Mitigate the threat, delight the customer

The average cost per attack across all sectors is £35,000, including mitigation costs. On paper, this looks like a figure that larger businesses should be able to handle on a one-off basis, but with a growing trend for repeated attacks (20% of victims experience a second attack within 24 hours), even wealthy companies are having to take note.

For the igaming sector, successful prevention is everything and so the choice of hosting partner is vital. Sure understands this and has designed and deployed a unique dual-island data centre network that offers the levels of resilience that operators need.

Sure’s vast experience in the igaming sector has informed the firm’s decision-making as it looks to develop its global presence in the industry. The company is determined to maintain its reputation for igaming network security and so has combined the physical resilience of island-based data centres with Arbor DDoS protection, which secures the high bandwidth gateways at the network’s edge.

As a result, our customers have peace of mind knowing that regardless of the size of attack, whether it’s a disgruntled 1000Mbps or a monster 1Tbps, their network will remain available and their customers loyal.

COMPANY PROFILE

•NAME SURE INTERNATIONAL •FOUNDED 2013 •SECTOR ONLINE CASINO •WEBSITEINTERNATIONAL.SURE.COM

Revolutionary technology – no matter the industry – must undergo the process of gradual acceptance and deal with the various challenges posed in its transition from concept to viable everyday use. We’ve seen over the past two years or so that blockchain has certainly followed this path in the gaming industry. Importantly, though, it’s this ongoing interrogation by industry peers that ensures disruptive products develop the characteristics that give them their longevity at the end of this phase.

FunFair Technologies has been championing blockchain’s inclusion in our industry for a while now; indeed, we had first-hand experience of dealing with these challenges on our path to going live with a shippable product earlier this year. It is through these hurdles and learning processes that we, and our competitors, have pushed the conversation on from ‘What is the blockchain?’ to ‘Where does your blockchain service sit with our needs?’

Those pushing the technology have had to see out various hindrances on the way. Externally, there was the crypto boom of late 2017, followed by a crash and period of uncertainty soon after. There were, and remain, mixed reactions to the blockchain from some regulatory bodies in gaming and finance, while the ambiguous security-versus-utility debate rages on.

Closer to home, the onboarding process for blockchain technology and cryptocurrency acquisition hasn’t had quite the same progression into the day-to-day use that some may have hoped for. Meanwhile, as was to be expected, many in our industry remain reluctant to embrace new technology, no matter its potential benefits to them.

However, it’s testament to the progressive sector we work in that we’ve come, in a relatively short space of time, from an embryonic idea based on the fairness that comes intrinsically with the blockchain to a fully-fledged sub-industry that services a global audience of many millions. Even more so, it’s pleasing to be able to use the trade press medium to delve into the intricacies of the technology and its working nature nowadays, rather than offering another blockchain education piece.

But it’s this next phase of blockchain that will see its true potential come to the fore, and its lack of comparable technologies as use cases makes this an exciting time for the gaming space.

Something that has separated many blockchain companies from traditional fiat platform providers is the ready-made community developed during and post token sale. For potential clients, this ready-to-use pool of potential players and advocates who want to use the technology as soon as it’s available should not be underestimated.

It would have been more straightforward to deliver our platform direct to those in the community, ignoring KYC procedures and licensing requirements in the name of a quick buck, as opposed to positively disrupting the gaming industry from the ground up in a correct manner.

Blockchain gaming’s major challenge, however, almost certainly lies beyond this existing, open community. When talking to prospective partners, the benefits of blockchain’s player protection and lower cost as a platform are understood, but what we need to do, and are in the process of doing, is explaining and demonstrating why the non-crypto player would want to make the leap to the decentralised world.

The success of this will likely come from two sides. First, further blockchain adoption by a global audience. As use cases enter more routine, day-to-day transactions, the education process will continue and the leap into the crypto-unknown will become a mere step, arguably similar to how PayPal rose to prominence with online transactions.

The secondary part of this persuasion of the day-to-day gambler has to rest on us, the blockchain stakeholders in gambling. We must provide the experiences, products and tools that they’ve come to expect. Online casino gaming has embraced the likes of video games and cinema to turn its own experiences into an immersive, retentive and enjoyable one, and blockchain technology shouldn’t be comfortable with offering anything less than this just because it’s later to the party.

Blockchain suppliers and casinos must channel the best of what’s already out there – we know what players demand – and improve on them with the various benefits of the technology.

I’d like to think of this as the end of the first phase of blockchain’s amalgamation into the wider gaming space. We, as a blockchain collective, want to deliver a better experience to players through blockchain-powered casinos and tools, and we must keep on raising the bar, running to the consumer where we can to ensure a better online gaming industry for all.

Jez San is a British technology entrepreneur and investor whose pioneering work in the field of real-time 3D computer graphics led to him being awarded the OBE for services to the computer games industry. He has since gone on to found companies including 3D online poker room PKR and most recently blockchain casino provider FunFair Technologies.

When American mathematician Claude Shannon published his paper ‘Programming A Computer For Playing Chess’ in 1950, it would have been difficult to imagine the sophistication of today’s artificial intelligence (AI) and its seeming omnipresence in our business and personal lives.

Shannon demonstrated extraordinary foresight with regards to the possibilities this technology would bring to the world. Introducing the potential of a chess-playing computer, he said at the time, “Although perhaps of no practical importance, the question is of theoretical interest, and it is hoped that a satisfactory solution of this problem will act as a wedge in attacking other problems of a similar nature and of greater significance.”

He envisaged several potential applications for the technology:

1. Machines for designing filters, equalisers, etc.

2. Machines for designing relay and switching circuits.

3. Machines to handle routing of telephone calls based on the individual circumstances rather than by fixed patterns.

4. Machines for performing various symbolic (non-numerical) mathematical operations.

5. Machines capable of translating from one language to another.

6. Machines for making strategic decisions in simplified military operations.

7. Machines capable of orchestrating a melody.

8. Machines capable of logical deduction.

Looking back at his technological forecast from a modern perspective, it’s clear Shannon was a true visionary, with many of his predictions having long since been brought to fruition.

The chess test

In 1997, IBM’s Deep Blue became the first computer system to defeat a reigning world champion in a chess match, beating Garry Kasparov before being retired by its development team. The complexity of chess and its seemingly infinite number of possible moves made this a watershed moment for AI, and one that was hard-won: almost half a century had elapsed between Shannon’s original conception of a chess-playing computer and Deep Blue’s eventual triumph.

Of course, the computers of Shannon’s day were incapable of dealing with the quantities of data we’re accustomed to now, and learning to intelligently play chess required systems to deal with an almost endless number of variables. Shannon calculated a conservative lower bound of the game-tree complexity of chess (ie the number of distinct games that could conceivably be played) of 10120, or 1 followed by 120 zeroes.

For comparison, there are generally estimated to be around 1080 atoms in the observable universe. Clearly then, building a computer able to consider even a fraction of these variables was a monumental challenge, and the 47 years that elapsed between the publishing of Shannon’s paper and Kasparov’s defeat should be considered relatively rapid progress. In fact, Deep Blue’s developers, among others, were laying the foundations for an ultra-accelerated technological boom this century, during which the capabilities of AI would be compounded and increase exponentially.

Building on the chess success

Chess is an extremely sophisticated game, but in recent years computer programmers have overcome even greater challenges.

The apparent simplicity of the ancient Chinese board game Go, which doesn’t feature a range of pieces moving in different ways like chess, may lead some to believe this would be an easier game to program a computer to play. However, Go is estimated to have a game-tree complexity of around 10360, meaning there are some 10240 times as many possible games as there are in chess.

Clearly then, Go was a worthy challenge for Google’s DeepMind developers, whose program AlphaGo became the first computer to beat a human professional player without handicaps on a full-sized 19×19 board in 2015. In less than 20 years, developers had gone from a computer mastering chess with its game-tree complexity of 10120, to mastering Go with its complexity of 10360.

The number of variables that AI is finding its way around is increasing exponentially and shows no sign of slowing down. The DeepMind team has suggested that AlphaGo is a step towards creating algorithms that can intelligently tackle some of today’s greatest scientific challenges, from designing new medicines to accurately modelling the effects of climate change.

Bots ’n’ big blinds

Last year, an AI-based computer program named Libratus was able to beat some of the world’s top poker players, prompting one to claim he felt the machine “could see my cards”.

This achievement involved further layers of complexity when compared to chess and Go, due to the inherent characteristics of poker. Firstly, chess and Go are both skill-based games with minimal elements of chance, whereas poker is a much subtler mix of the two.

In chess and Go, players also have access to complete information about the game: the pieces their opponent has, the moves they have already made, what moves are available to each player, and so on. But in Texas Hold’em, the information offered to both parties is incomplete, and while they can both see what’s on the flop, turn and river, the absence of information about your opponent’s hand is what makes the game worth playing (thanks, Captain Obvious).

Furthermore, when considering the use of bluffing and elements of randomness in both betting strategy and cards dealt, we can begin to appreciate some of the problems facing developers in creating a poker-playing bot that can keep up with human play, let alone that of a top-ranked professional.

Libratus’ success was made possible through machine learning, the process by which the bot is able to ‘practise’, playing against itself and refining its strategies. Clearly, the millions of simulated hours the machine dedicated to this were enough to outsmart even the world’s most formidable players.

Machine learning allows AI systems to constantly adapt to new information, change their strategies and effectively analyse action that has already taken place. In fact, it may have been Libratus’ continual learning between games, and its analysis of information from the tournament’s first few days that allowed it to refine its strategies and emerge victorious.

This year, the bots have stepped up once again and are now taking on the world of esports under the watchful eye of billionaire schoolboy Elon Musk. OpenAI Five is an artificially intelligent esports team, which in August played in DOTA2’s The International, the world’s largest professional tournament in one of esports’ most sophisticated titles. And OK, it didn’t win. Yet.

Thus far, the OpenAI team has shown a few less-than-ideal playing strategies but they have held their own overall. Their first match in The International saw the bots face off against pro team paiN, in a close-fought battle lasting more than 45 minutes. While a victory would surely have demonstrated the program’s superiority over human players, its ability to at least give them a run for their money should tell us something about AI’s dynamism in 2018. There are incalculable variables involved in a game like this, which is played between two teams of five choosing from over a hundred characters, each with unique abilities, in a huge virtual arena. The ability of a machine to adapt to the unexpected demonstrates its human-like cognitive abilities, and raises further questions of where this tech may take us in the future.

During the training process, OpenAI Five bots are capable of simulating 180 years of experience (over 1.5 million hours) each, every day. That’s more than 900 years of experience, daily, that the team amasses. Given the old adage that it takes 10,000 hours to become a true expert at something, what will machines that have had 10,000 years’ experience or training be capable of in the future?

Given the exponential rate of growth in this area, will it be possible for the machines of the future to simulate hundreds of thousands or even millions of years’ experience, every day?

What’s the big idea?

So, what does this mean for the gaming world? Integrity ought to be a major concern here. As AI technology becomes more widely adopted and available, what systems will be put in place to prevent online poker players from running an AI bot alongside their virtual table, providing them with the moves that will always give them a statistical advantage? Will the fraudsters of the future enter into amateur esports competitions equipped with bots that have effectively trained for thousands of years?

Perhaps new systems will be developed to determine when an AI bot is masquerading as a human, but how soon will this become a pressing need for the gaming industry?

Will applications advance on both sides to create a kind of technological arms race?

Bots playing online poker are already a concern for recreational players, though the sophistication of these is typically quite far from the dizzying heights of Libratus. Many more accomplished online players feel they’re able to identify when they’re playing against a bot, and some claim the ability to exploit their idiosyncrasies for profi However, does this act as a barrier and prevent non-players from getting involved? If the overarching view of online poker is that there are people out there using complex algorithms to cheat amateurs out of their hard-earned money, new players will surely be put off and opt for a less risky game to play.

So how can operators tackle this? You guessed it – more AI! Increasingly accurate personal identification solutions are helping operators to know their customers more intimately than ever, and in-depth data analysis can give them a great deal of insight into how those customers play. By strictly verifying each customer’s identity and analysing their playing styles, operators should be able to protect their honest players while eliminating the threat of them being thrown to the technological sharks.

Whatever happens next, it’s clear that no company can turn a blind eye to advances in AI technology. If it isn’t used for maintaining integrity and responsibility in gaming, we can be sure that someone out there will use it for precisely the opposite purpose.

Scientific Games has revealed plans to launch an initial public offering for a minority stake in its social gaming division.

The business, comprising social casino apps including Jackpot Party, Bingo Showdown and Monopoly Slots, has consistently grown. The company first moved into social in 2013 through the acquisition of WMS, which had launched Jackpot Party a year earlier.

In the business’ results for the third quarter of 2018, revenue from social was up 11% year-on-year to $105.1m, with adjusted EBITDA climbing 34% to $27m.

The quarter also saw monthly active users rise 6% to 8.4m, with average daily revenue per daily active user climbing to $0.43. The division has also succeeded in shifting to a mobile-first business, something that competitors such as Zynga struggled to do, with 79% of revenue coming through the channel in Q3.

“We believe an IPO would provide greater flexibility to pursue additional growth initiatives, specifically designed for our social business as well as unlocking additional value for Scientific Games’ stakeholders,” Scientific Games chief executive Barry Cottle explained.

Cottle added that the social was the only business unit that merited being spun off, as a result of it being the only customer-facing division. All others, were B2B-focused, with technology and solutions interlinked, making it harder to separate each into distinct entities.

Money raised through the IPO is to be used to pay down the supplier’s long-term debt, which stood at $8.7bn

Most read on iGamingBusiness.com

1) Gibraltar wins Spanish support for gambling future

2) UK raises remote gambling duty

3) Unibet expecting chess final bonanza

4) William Hill tables £242m offer for MRG

5) Ladbrokes may face mass payout on ‘cancelled bets’

2) Grant Williams quits Hills ahead of online overhaul

3) Unibet rapped for ‘sponsored’ Henderson tweet

In their own words…

“It’s this ongoing interrogation by industry peers that ensures disruptive products develop the characteristics that givethem their longevity”

JEZ SAN, FUNFAIR, PAGE 18

“Marketing departments are being asked to do a lot more, and haven’t seen pay rises to reflect theincreased workload”

GARETH MULLEY, PENTASIA, PAGE 55

“[The sector] contains most of the ingredients necessary to make investors potentially view [it] as something of a dog”

PAUL LEYLAND, REGULUS PARTNERS, PAGE 111

In numbers

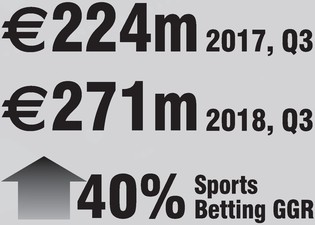

The French iGaming market, the source of huge excitement when it opened in 2010, has since been held up as an example of what not to do when re-regulating a gaming market. Hefty taxes have made it almost impossible for many to turn a profit, leading to an exodus of operators. However, things seem to have taken a turn for the better. Poker, following years of decline, has recovered, due in part to the launch of liquidity sharing with Portugal and Spain. Industry efforts to revitalise horse racing are paying off. And the French betting public has fallen in love with sports betting. The vertical began life as an afterthought, but has now climbed to the summit of the market, and growth shows no signs of slowing. It remains to be seen what regulatory changes will be prompted by the government’s sale of its majority stake in La Française des Jeux, but some suggest that it may finally see the market expanded beyond the three legal verticals. The operators that have exited the market may soon be considering moving back in.

GOOD TIMES

THE STARS GROUP

The operator formerly known as PokerStars has long profited from its absolute dominance of the poker vertical, but it has had the foresight to realise the importance of diversification. This has seen it make almost as big a splash in online casino as it made in its core vertical, but sports betting, via the BetStars brand, has proved a trickier nut to crack. A multi-billion dollar M&A splurge later, however, and The Stars Group has seemingly resolved all its betting-related inadequacies. Group revenue soared to $572.0m for Q3, with Sky Betting and Gaming and the Australian BetEasy businesses helping the contribution from sportsbook to jump from $11.7m to $154.8m. While increased operating expenses resulting from the acquisitions almost wiping out profit for the period, it’s a sign of The Stars Group’s strength that it can complete two major acquisitions and still post a positive result.

BAD TIMES

SPORTECH

Having gone from issuing a profit warning to losing its chief executive in a week, Sportech is facing tough times. This, ironically, is happening during a period where everything it had appeared to be working towards should be coming to fruition. In recent years the company has appeared to be positioning itself to be an early mover in the US sports betting market, but with PASPA a thing of the past, it has quickly been outstripped by larger, more nimble peers. This has culminated in a warning that full-year EBITDA would fall up to 10% below its projections, as a result of “certain expected sales contracts” not being signed. Now chief executive Andrew Gaughan, with the company since 2004, has announced his departure just months after taking the top job. When Gaughan took on the role the company said it would no longer entertain offers from prospective acquirers. It’s now banking on sports betting being legalised in Connecticut – if it fails to make a splash in that market, it may soon be back to looking for buyers.