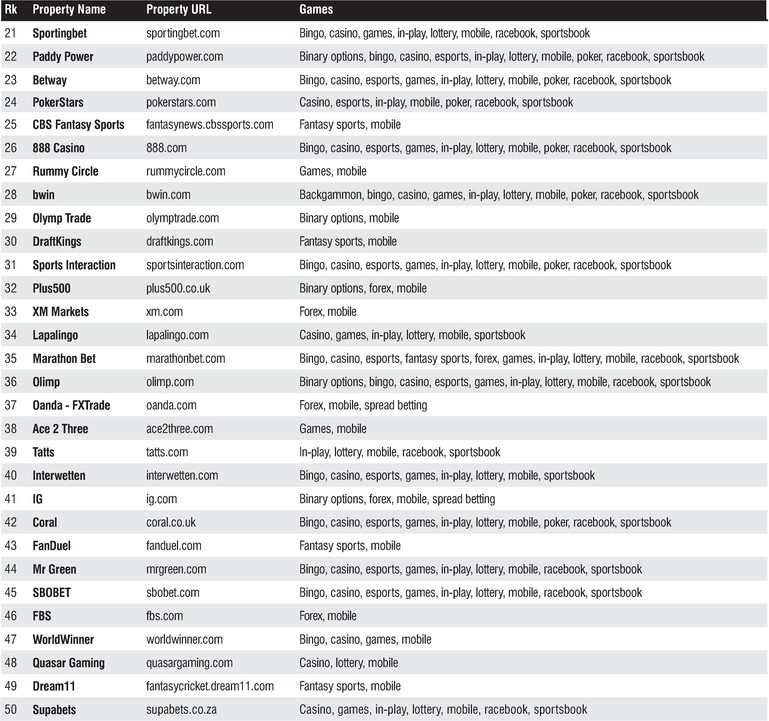

• Traffic rankings indicate relative popularity of the 100 most popular igaming sites offering real-money wagering and are based on historical web usage of a panel of nearly 20 million users over a three-month period prior to publication.

• The rankings are estimates based on panel usage and should not be considered absolute ranking values.

• Only the top 5% of all igaming sites are listed. For detailed, current, accurate information on 2,500 igaming sites and 2,000 igaming portal sites, along with rankings of the top 1,000 igaming sites and the top 1,000 igaming portals, directories of software providers, other suppliers, regulatory jurisdictions and more, the latest edition of Casino City’s iGaming Business Directory is indispensable.

H2 Gambling Capital is the gambling industry’s leading consulting, market intelligence and data team. They have a track record of more than 15 years focused on the global gambling industry. All of the detailed data and the right to re-publish extracts is available via H2’s Global Data and Market Intel Service.

H2 Gambling Capital is the gambling industry’s leading consulting, market intelligence and data team. They have a track record of more than 15 years focused on the global gambling industry. All of the detailed data and the right to re-publish extracts is available via H2’s Global Data and Market Intel Service.

Operator type: centralised igaming system via Delaware Lottery and operated by the three state casinos

Go-live date: October 2013 On 31 October, 2013, Delaware became the first state to launch a full service online gaming offering. The igaming program is run by the state lottery and powered by a vendor collaboration between 888 and Scientific Games/WMS. Delaware’s 888-powered poker sites, including WSOP, began pooling liquidity with Nevada’s in March 2015. This was extended to include New Jersey on May 1, following October 2017’s Multi-State Internet Gaming Agreement (MSIGA). On June 5, Delaware became the first state to launch sports wagering following the lifting of the federal ban when Delaware Park, Dover Downs Hotel & Casino and Harrington Raceway & Casino started offering sports betting services. Delaware, which had been offering parlay NFL wagering via partial exemption under PASPA, is yet to confirm whether it will allow betting on college sports events. State lottery regulations currently ban any bets being taken on Delaware’s two Division I colleges (Delaware State and the University of Delaware).

Nevada:While

Regulated gaming type: poker

Operator type: applicants with existing landbased licences

Go-live date: April 2013 There are two real-money online poker platforms in operation in Nevada: WSOP and Real Gaming, formerly South Point Poker. WSOP started to pool liquidity with Delaware in late March 2015 and on May 1 started doing so with New Jersey, following the MSIGA signed by the three states in October 2017.

Go-live date: November 2013 The sites on the Golden Nugget licence — Golden Nugget, Betfair, Playsugarhouse, Resorts, PokerStars and Mohegan Sun — extended their share to 35.3% of the market. A bill authorising sports betting became law in June this year, with the first bets taken on June 14. The first mobile sports betting application went live on August 6.

Georgia: Green

Green Regulated gaming type: online lottery

Operator type: Georgia Lottery monopoly

Go-live date: November 2012

Illinois:Green

Green Regulated gaming type: online lottery

Operator type: Illinois Lottery monopoly

Go-live date: March 2012 The Illinois Lottery has stayed online despite lawmakers failing to reauthorise the four-year pilot programme that expired in March 2016. An amendment to legalise igaming, sports betting and DFS failed to pass the Illinois House Executive Committee as part of a casino expansion bill in late May. Lawmakers held a hearing in October to discuss the legalisation of sports betting. At least one new bill will be introduced in January. Extending authorisation to online and mobile operations has remained part of the discussions.

Kentucky: Green

Green Regulated gaming type: online lottery

Operator type: Kentucky Lottery monopoly

Go-live date: April 2016 A bipartisan group of legislators is close to finalising a sports betting bill, which it plans to pre-file prior to the start of next year’s legislative session. The legislation will reportedly include mobile and online wagering, as well as betting at brick-andmortar facilities. The nine-member working group has reportedly also agreed to forgo an integrity fee and to tax net revenues as opposed to handle, as provided in Senator Julian Carroll’s previous bill from June. Three sports betting bills have been introduced in the state legislature, none of which have passed a committee vote thus far. Senator Morgan McGarvey predicted that the odds of the most recent bill passing when the General Assembly meets next in January are “good”.

Michigan: Green

Green Regulated gaming type: online lottery

Operator type: Michigan Lottery monopoly

Go-live date: August 2014 The House passed a bill in June that would allow the state’s casinos to offer various forms of gambling, including poker and sports, over the internet. It hoped that the bill would be a top priority in the Senate in the fall, but unresolved issues — including constitutional questions and stalling negotiations between tribal and commercial operators — have slowed the measure’s progress.

New Hampshire: Green

Green Regulated gaming type: online lottery

Operator type: New Hampshire Lottery monopoly

Go-live date: September 2018 New Hampshire commenced sales of lottery tickets online in mid-September, making it the latest state to offer lottery over the internet.

Pennsylvania:Green

Green Regulated gaming type: online lottery

Operator type: Pennsylvania Lottery monopoly

Go-live date: June 2018 The only type of gambling currently offered online in Pennsylvania is the lottery (instant win games only), but casino games and sports betting are forthcoming. Pennsylvania became the fourth state to fully legalise online gambling in October 2017 after Governor Tom Wolf signed an expansive gambling package into law. The legislation allows for the regulation of online poker, slots and table games within the state’s boundaries. Additionally, the Gaming Control Board is now issuing sports betting licences. Onsite sports wagering will likely commence in late fall. Mobile betting on sports will be permissible but only available to participants located within a licensed casino. 10 of the state’s 13 approved casino operators have applied for licences in at least one of the four categories. 1 interactive gaming licences (five online poker, three online slots and three online table games) remain up for grabs among licensed operators. Each interactive gambling licensee is allowed to partner with multiple interactive platforms.

Connecticut: Amber

Present status: In March both the state’s gaming tribes, the Mashantucket Pequot and the Mohegan, came out in support of legalising online gambling and sports betting. Executive director of online gaming for the Mashantucket Pequotowned Foxwoods Resort Casino, Seth Young, in written testimony to a Public Safety and Security Committee hearing said: “The strongest opportunity for the state is in legalising state wide igaming, another activity that is currently operating for Connecticut residents in the black market.” Avi Alroy, VP of interactive gaming for Mohegan Sun, said online casino gaming and sport wagering would “reduce unregulated bets that are done locally and offshore and increase state revenues.” Both also submitted estimates to the committee that online gambling would generate around $87m in tax revenue to the state over its first five years of operation, based on a pragmatic tax rate and legalisation of casino and poker.

Massachusetts: Amber

Present status: A measure introduced by Senator Eileen Donoghue in January would regulate online gambling and daily fantasy sports as well as create a commission to study online sports betting. In June the Senate authorised the Joint Committee on Economic Development Emerging Technologies to investigate and study the issue. Efforts to fast track the omnibus bill fell short in 2018, but Joint Committee Chairman Rep. Joe Wagner believes the initiative will be up for a vote in 2019. Gov. Charlie Baker has confirmed that sports betting will be addressed in January.

Missouri: Amber

Present status: At least three bills to authorise sports betting have been introduced to the legislature, two of which include provisions to allow sports betting over the internet. Lawmakers have conceded that it is unlikely any of the bills will pass in 2018 but are hopeful for 2019.

Kansas: Amber

Present status: Multiple bills to authorise sports betting, including provisions authorising online sports betting, were introduced to the legislature in 2018. Under the proposed bills, the Kansas Lottery would have a master license, with approval to enter into contracts with lottery and racetrack gaming facilities. All of the bills died in committee, but proponents are hopeful they will gain traction in 2019.

West Virginia: Amber

Present status: Hollywood Casino at Charles Town Races took its first legal bet on sports on August 30. The state, the fourth Alabama to of launch PASPA, sports enacted betting its sports since betting the repeal law in March 2018. Hollywood Casino is one of five West Virginia casinos, with the other four expected to go live with sports betting this fall. Under the new law, casinos can offer online and mobile wagering, which could be available in West Virginia by late fall. Use of apps for remote electronic gambling will be limited to patrons located physically inside state borders.

Louisiana: Red

Present status: A bill introduced this year in Louisiana would legalise online gaming Georgia parish-by-parish basis via a voter referendum. The bill is unclear on what types of gambling would be authorised and makes no mention of taxation or licensing fees. Even if the measure progresses, the state would not see live authorised online gambling until at least 2020.

New York: Red

Present status: Online poker, this time alongside sports wagering, failed to make the final budget proposal for the third year running, with Senate support again not mirrored in the Assembly.

There was no uniform approach to the handling of complaints by, and disputes with, customers in gambling until the provisions of the Gambling Act 2005 came into full effect in Great Britain in September 2007.

It was only then that gambling debts became legally enforceable for the first time. The UK Gambling Commission’s early versions of its Licence Conditions and Codes of Practice (LCCP) did little more than require licensed operators to have a written procedure for customer complaints and disputes and to keep a record of them.

When the first requirement for operators to refer disputes to an independent third party was subsequently introduced, it wasn’t even mandatory for it to be free of charge for the customer.

How times have changed. The consumer has increasingly been promoted to the heart of gambling regulation, most prominently during the relatively short reign of Sarah Harrison as chief executive of the Gambling Commission. Harrison’s arrival also coincided with the Alternative Dispute Resolution for Consumer Disputes (Competent Authorities and Information) Regulations 2015 coming into force.

This combination of events led to the Commission’s “Complaints processes in the gambling industry” review in March 2017. This was conducted against a backdrop of heavily publicised concerns on the part of the Commission about what it perceived to be an increasing lack of public trust in gambling operators, something that has sadly grown apace since then.

It included a finding that “the complaints system in the gambling industry is not working for consumers, who have found it difficult to access, time-consuming to use, and [who] question whether it is independent and transparent”.

In her foreword to that document, Sarah Harrison said: “We want to see an industry that aspires to excellence in complaints handling.

An industry that values and seeks out feedback from customers, that swiftly and effectively resolves customer complaints, and that uses the learning from those customers to raise its standards and deliver ever higher levels of customer service”.

So it is that, with effect from 31 October 2018, a new complaints and disputes regime comes into force in each of the following respects.

1)LCCP change

An amended social responsibility code provision 6.1.1 within the LCCP comes into force on that date, intended to ensure that B2C gambling operators provide better complaints processes, including arrangements for their customers to be able to refer any dispute to an alternative dispute resolution (ADR) provider, if the operator has been unable to resolve it within eight weeks from receiving it.

2) Gambling Commission guidance

UK licensed operators will be mistaken if they think that the above change needs little preparation. The Gambling Commission has produced seven pages of guidance on implementation of the amended LCCP provision (available on its website) that it expects licence holders to take account of when developing their complaints handling policies.

The guidance document is essential reading material. It sets out the minimum standards that the Commission expects from operators when they handle customer complaints and summarises the Commission’s reporting requirements relating to complaints that operators receive.

Addressing past confusion about whether an ADR provider has jurisdiction to adjudicate certain matters referred to it, the guidance also provides much-needed clarity on what the phrases ‘complaint’ and ‘dispute’ mean, namely:

• ‘complaint’ means an expression of dissatisfaction, whether spoken or written, about any aspect of the way the licence holder conducts its licensed activities (including the outcome of a gambling transaction, the way in which the transaction was managed and concerns about the way in which the licence holder conducts its business in relation to the three licensing objectives) and

• dispute’ means complaints about the customer’s gambling transaction (including management of it) that have not been resolved at the first stage of the complaints procedure, including those linked to the application of bonus offers or to other terms and conditions, account management, or the customer’s ability to access his or her funds and winnings.

The guidance also includes very helpful flowcharts illustrating the applicable complaints process timescales and complaints and disputes regulatory return requirements.

3)Standards and guidance for ADR providers

The Gambling Commission has published new standards and guidance for ADR that are intended to improve how complaints are handled by ADR providers in the gambling industry. This follows the Commission’s finding in March 2017 that consumers did not always get good customer service from ADR providers and that decisionmaking standards varied.

It would be a mistake for operators to think this guidance is applicable solely to ADR providers. The new standards and guidance make clear the Commission’s expectations on:

• the types of consumer complaints it expects ADR providers to take on (including disputes linked to unfair terms or practices),

• principles for considering compensation,

• decision quality standards, particularly focused on how providers look at and use evidence,

• the Ombudsman Association’s six principles of good governance that it expects ADR providers to follow,

• conflicts of interests,

• the information and customer service ADR providers give to consumers (including a reminder that all gambling businesses that sell goods or services to consumers online must provide on their websites a link to the ODR platform) and

• the information and data ADR providers share with the Commission and others, each of which are very relevant considerations for operators.

The aforementioned definitions of ‘complaint’ and ‘dispute’ make it clear that complaints that are not related to the gambling activities and do not pose a risk to the licensing objectives do not fall within the scope of ADR provision within the Commission’s regulatory ambit.

There may of course be borderline cases, for example a complaint about poor customer service or staff manning a telephone or online chat. While that might not appear at first sight to be gambling-related, it might well be if the poor service makes it difficult or impossible for the consumer to promptly raise concerns or make a complaint.

The Commission suggests that “where the type of complaint is unclear, it is generally better to at least initially treat it as a gambling-related complaint”.

The British have a reputation for complaining. Licensed gambling operators need to ensure those complaints are all handled properly in accordance with the new requirements.

David Clifton is a founding director of Clifton Davies Consultancy Limited and a consultant to Joelson Wilson Solicitors. David has specialised in gambling law since the early 1980s and was among the first UK lawyers to advise the online gambling pioneers in the mid-1990s.

“Storm clouds” are gathering over the industry and are in danger of bursting – so said the Gambling Commission’s representative at an industry conference last month.

Just a couple of weeks earlier, the Gambling Commission’s executive director confidently predicted, at a seperate industry conference, that the escalation of Gambling Commission fines, which have increased more than eleven-fold from £1.6m to £18m in the last year, is set to continue.

These are portentous statements, and the message for the gambling industry in the UK is clear. Regulation has become tougher, and it will continue to get tougher, unless and until the industry can bring about change in the current negative public, political and regulatory narrative.

The Gambling Commission’s warnings come on the back of a stream of sensationalist headlines from the mainstream press – the Sunday Times front page headline “Gambling sites forced to stop luring children” being one example. With public concern having been whipped up and put in the spotlight by press campaigns, MPs have also become increasingly engaged in anti-gambling rhetoric and policymaking.

To complete this connected cycle of events, regulatory authorities including the Gambling Commission, the Advertising Standards Authority (ASA) and the Competition and Markets Authority (CMA), have come down hard on the industry with concrete regulatory action.

This has included CMA undertakings on bonus promotions, wagering requirements and restrictions on withdrawals, tougher new UK gambling advertising standards and a number of harsh ASA rulings.

Most topically, the Gambling Commission’s new Social Responsibility Code provisions came into force on 31 October. These new requirements mean that (among other things) a breach of the UK advertising codes, or sending direct e-marketing without specific and informed consent, will constitute a breach of the operator’s gambling licence.

A breach opens up the full range of regulatory sanctions including unlimited fines and licence suspension and revocation, which stands regardless of whether the offending activity was conducted by the operator itself, or by an affiliate without the operator’s approval.

In the press and in Parliament, the principal area of focus is currently pre-watershed gambling advertising on television, mirroring similar campaigns in Australia, Belgium and Spain – and, of course, in Italy, where a far broader blanket ban will soon come into force.

It must be said that the gambling industry has not been an entirely innocent victim. I think many readers would concede that parts of our industry have been slow to react to regulatory mood music over a period of time, have not always reached the high standards of compliance they would expect of themselves, and have not necessary helped themselves in the way they have sought to justify certain activities – the FOBT maximum stakes debate being an example of the latter.

Making progress

However, the industry’s tone and approach has changed markedly over the last year, with abundant examples of lessons having been learnt. From what I have seen, the industry has increased its focus on compliance yet further, increased its emphasis on (and investment in) responsible gambling, and is taking more positive steps to influence the debate, including offering qualified support to the idea of tighter restrictions on pre-watershed television advertising.

The industry has got the message, and is working hard to improve its image. If it is to succeed in doing that, and go the way of the alcohol industry rather than the tobacco industry, it will need objectivity and rational, evidence-based decision making from those that matter most.

That may be too much to expect from certain elements of the mainstream press in the short term, but it should not be too much to ask of the regulators. In Britain, the Gambling Commission should support the industry not just to comply but also to grow, and should regulate in a proportionate and risk-based way. Now more than ever it is crucial for the industry that the Gambling Commission keeps those principles in mind.

One area where this will be particularly pertinent is in enforcing the new social responsibility code relating to breaches of the advertising codes. The ASA’s decision-making process is designed in the context of its own relatively limited sanctioning powers, and can throw out unpredictable and somewhat subjective results. It is therefore crucial that the Gambling Commission takes a selective and proportionate approach to pursuing operators for adverse ASA rulings. The Commission has said it will do just that, which is a positive sign.

There are other ways in which the Gambling Commission could contribute to the restoration of objectivity and evidence-based decision making in public debate. As well as pre-watershed television advertising, there has been vociferous criticism of the use of cartoon characters in games. What these two issues have in common is they are easy targets for the press and politicians: they look bad. But are they actually the areas in which regulators should be concentrating their resources, when there is little evidence of them causing harm?

Public concern about pre-watershed gambling advertising on television and its effect on children is genuine. However, according to Ofcom’s November 2017 report into media use and attitudes amongst children and parents, children aged 5-15 spend on average 14 hours per week watching television, compared to over 40 hours on the internet, mobile or gaming.

In a similar vein, do cartoon characters actually encourage children to start gambling, or are they rather less likely to appeal to 12-17 year olds who may be more drawn to content that is more “grown-up”?

Surely the best way to protect the young and vulnerable is not to get carried away with areas of press focus, but rather to maintain an objective, evidence-based approach and divert regulatory resources to areas which could be much more significant in minimising harm – unregulated skins betting, for example.

With the enforcement stakes being raised to unprecedented levels, the actions of the regulator — not just the industry — will come under increasing scrutiny.

Andy Danson is a partner in the commercial department at Bird & Bird and a member of the law firm’s media, entertainment and sport group based in London.

Much has already been written about the Gambling Commission’s September 2018 consultation on proposals to introduce new licence conditions. These include bolstering requirements for operators to verify the age and identity of customers before depositing and gameplay is permitted.

This was identified as a priority in March 2018, when the Commission published its Review of Online Gambling. Whatever the responses to the latest consultation, it’s inevitable that the Licence Codes and Conditions of Practice (LCCP) will be revised from April 2019 to bring these changes into force.

A more controversial proposal contained in the Commission’s Review of Online Gambling, which is referred to but not part of the consultation is the proposal to introduce mandatory limits on customers’ gambling activity.

The Commission has stated that it intends to consult “at a further date” on these proposals, which it considers will reduce gambling-related harm. Under the future proposals, operators will have to impose financial limits until further information about the customer’s financial means have been verified and an increase is justified.

Mandatory financial limits will represent a departure from the current method of giving customers the option to set limits on their own activity, to one introducing restrictions on deposits or losses by default.

Under the current LCCP and Remote Technical Standards (RTS), remote licensees must apply policies and procedures for customer interaction where they have concerns that a customer’s behaviour may indicate problem gambling. Such procedures must include interacting with customers who are showing signs of obvious and overt problem gambling — but also talking to customers who are not displaying those signs, by reference to time or money spent.

Specific player protection measures are required for high value or VIP customers. In addition, RTS 12 requires that customers must have the ability to set their own deposit or spend limits on registration, or at any time after registration.

Operators must offer financial limit facilities for periods of 24 hours, seven days or one month, and a 24 hour “cooling off” period (with subsequent confirmation by the customer) is required before an operator can increase a previously set limit.

When combined with “time spent gambling” notification requirements and the option to set reality checks, as required by RTS 13, there are already quite comprehensive measures in place to protect consumers.

However, crucially, the current measures are reliant on customers using these optional features to protect themselves from harm. Often it will be the very people who are at risk from gambling who will ignore these facilities and will carry on gambling regardless.

The Commission is now proposing that it will take matters out of the hands of consumers and will impose financial deposit or loss limits by default.

Prescribed limits

In the consultation, the Commission asks respondents to provide information or evidence of good practice that helps licensees to ensure gambling remains fair and safe. The Commission seeks evidence of both existing good practice and what measures are possible, with a view to formulating future proposals for mandatory account limits. Licensees, identity verification providers and gambling customers are encouraged to respond, with a view to influencing the future proposals.

At present, there is no indication from the Commission of what these mandatory account limits might be and when they would apply. For example, we don’t know yet if they would relate to deposits, spending or losses.

It’s possible that the same financial limits will not apply across the board, but that different customers could be allocated different financial limits for example, utilising postcode deprivation indices, economic data and credit searches. It’s possible that the Commission will consider imposing variable limits tailored to each customer.

The Commission asks for evidence of “risk factors” of harm, which can be detected early on in a relationship with a new customer, such as failed deposits at first attempt, use of high interest credit cards, large numbers of payment methods registered, bonus and void requests and patterns of play. It is particularly keen to hear from operators who have voluntarily applied limits to customer accounts and how effective those measures have been.

These proposals will be ringing alarm bells with some remote operators, particularly casino operators with a large number of “high value” or VIP customers. Staking and losses for these players are likely to far exceed any mandatory limits that may be imposed. Even if the default limits could be increased further down the line once more information is known about a customer’s financial means and behaviour, mandatory restrictions are likely to hit operators’ turnover and profits.

It’s interesting to note that these proposals are being progressed despite data published by the Gambling Commission itself which indicates that rates of problem gambling in the UK are static.

Of course, the Commission has an obligation to protect the vulnerable from harm, including those in this static group, but there is likely to be criticism in some quarters about the creep of the nanny state. While restrictions on products such as alcohol and tobacco can easily be justified as they are fundamentally harmful to health, the major risk of gambling addiction is financial.

For some, it’s quite a step to move from giving individuals options to monitor and rein in their gambling outlay, to preventing them from spending their own money however they wish. Clearly society needs to consider where we are heading with these types of proposals. Shopping can be addictive – if we follow this path, how long will it be before places such as car showrooms, handbag and shoe shops will be required to display warnings about irresponsible spending?

While a considerable number of individuals use gambling as a harmless leisure pursuit, there will always be people at the extreme end of any compulsive activity. The question is, what active measures are justified to protect those individuals from harming themselves?

Richard Williams is a partner and joint head of the gambling, licensing and regulatory team at Joelson.

WIGGIN is a law firm dedicated to supporting the media, entertainment and gaming sectors. Its market-leading betting and gaming group provides specialist legal services to an world’s leading gambling operators and suppliers and also enjoy helping entrepreneurial, interactive start-up businesses. If you’d like to hear more, contact us at gambling@wiggin.co.uk

Operator type: Licences for sports betting and horse race betting are available for private operators on a regional basis within Austria, whereas poker, casino, bingo and lottery are controlled by the monopoly, Casinos Austria, which has exclusive rights until 2027.

Status: In 2016, national courts reached conflicting decisions on the compatibility of Austria’s current gambling legislative framework with EU law, which remains unclear. The draft amendments to the Gambling Act, which would introduce ISP-blocking measures and an express provision rendering gambling contracts contrary to the Gambling Act void, has been temporarily withdrawn. It is unclear if the initial draft will be republished.

Operator type: All products are available to private operators except for lotteries, which are reserved exclusively for the monopoly provider. However, online operators need to partner with local casinos in order to satisfy the land-based establishment requirement; alternatively, apply for one of the 34 retail licences (F1 licences) that can be extended to cover online (F1+ licence).

Status: There remain valid arguments that the existing regime is incompatible with Belgium’s EU Treaty obligations. On 22 March, 2018, Belgium’s Constitutional Court ruled in favour of an exemption from VAT obligations for online gambling transactions. Active enforcement measures against operators and players are in place. The Belgian government recently approved a royal decree restricting advertising for online gambling, which is expected to enter into force in summer 2019.

BULGARIA

Regulated gambling products: Sports betting, horse race betting, poker, casino, bingo and lottery (excluding raffles and instant lottery games).

Operator type: All products are available to private operators except for lotteries, which are reserved exclusively for the monopoly.

Status: Any operator from an EU/EEA jurisdiction or the Swiss Confederation can apply for a licence. The Bulgarian regulator has awarded approximately 20 licences to date, including to a number of international operators. The government has notified the European Commission of draft amendments to the country’s gambling legislation which, among other things, would introduce stringent restrictions on how gambling products can be advertised. The standstill period ended on 15 October, 2018.

Operator type: All products are available to private operators except for lotteries, which are reserved exclusively for the monopoly provider. Private operators can only be licensed to offer igaming if they obtain a land-based casino or betting licence.

Status: Following Croatia’s accession to the EU in 2013, it was understood that it would submit new legislation that was compatible with EU law However, on 5 March, 2014, the Croatian government notified a draft bill to embolden the position of the monopoly and local operators, giving rise to further incompatibility issues. The receipt of a detailed opinion from the EC stalled the legislative process.

CYPRUS

Regulated gambling products: Sports betting, horse race betting and lottery.

Operator type: OPAP has a monopoly over lottery operations; sports-betting licences are available to private operators.

Status: Cyprus regulated online betting in July 2012, although a licensing regime was not established until 2016. Applications for online sports-betting licences were accepted for a one-month period only from 3 October, 2016. ISPs are obliged to implement blocking measures to prohibit Cypriot residents from accessing unlicensed gambling websites. Cyprus has notified new draft gambling legislation to the EC in response to concerns about the local establishment requirement under the Betting Law and the equal treatment of gambling operators in the country (principally as a result of the exemption afforded to OPAP).

Operator type: EU and EEA-based operators are able to apply for licences.

Status: The new gambling regulatory regime entered into force in the Czech Republic on 1 January, 2017, allowing EU/EEA companies to enter the market. The licensing regime has been called into question after a number of foreign operators are believed to have withdrawn from the licensing process, citing the current regime as being incompatible with EU law ISP-blocking measures are active in the jurisdiction.

DENMARK

Regulated gambling products: Sports betting, fantasy sports, horse race betting, poker, casino, bingo and lottery.

Operator type: Sports betting, poker and casino licences are available to private operators. Lottery is controlled by the state monopoly.

Status: The Danish online gambling regime went live on 1 January, 2012. ISP-blocking measures are active in the jurisdiction and the Danish Gaming Authority has been granted an injunction to block operators and suppliers that have been targeting Danish customers without the requisite licence. Danish political parties have reached an agreement to introduce limits on bonuses. The Ministry of Taxation is understood to be aiming for a 1 January, 2019 implementation, although the exact proposed changes are currently unknown.

Operator type: Licences for all gambling products are available to private operators save for lotteries, which are reserved exclusively for the monopoly operator.

Status: Operators seeking to accept business from players in Estonia must be issued an activity licence for the type of gambling they wish to offer, then an operating permit to provide the services remotely. A blacklist of about 1,100 operators is maintained and updated by local authorities and ISP and payment blocking is in force. Though some operators argue that the regime is still not compatible with EU law, there has been no open challenge by the EC to date.

Operator type: All gambling products are under the exclusive control of monopoly provider Veikkaus Oy.

Status: Despite the existence of a national monopoly, EC enforcement action has been dropped subsequent to various changes to Finnish laws. Active enforcement measures are in place (restrictive marketing for offshore operators and ISP blocking).

Operator type: Private operators can obtain online licences for sports betting, horse race betting and poker. The monopoly has exclusive rights to bingo and lottery.

Status: A regulated market since the introduction of a licensing regime in 2010, following which the EC withdrew its infringement proceedings. Parliament has given its formal approval to plans to privatise the state-owned operator of France’s national lottery games, Française des Jeux (FDJ), with broader regulatory changes to the online sector expected to follow.

GERMANY

Regulated gambling products: Schleswig-Holstein, a small northernGerman state, regulates sports betting, horse race betting, poker, casino and bingo. The other 15 states of Germany currently permit only sports betting and horse race betting.

Operator type: Private operators can no longer obtain licences in Schleswig-Holstein and those in existence will expire on 30 June 2019. In the other 15 states, horse race betting licences are available at a regional level but the position surrounding the 20 available sportsbetting licences is still uncertain.

Status: The main legal framework for gambling regulation in Germany has been the subject of much debate and has been heavily criticised by the European Commission and interested parties/states within Germany for a number of years. Its legal standing is highly questionable, particularly in light of a decision of the CJEU (in Sebat Ince, 2016), which found the sports betting tender process to be incompatible with EU law and called into question the restrictive remote gambling regime in general. The decision led to calls for comprehensive legal reform of Germany’s gambling legislation. In March 2017 all 16 German states signed amendments to the country’s gambling law; however, on 22 September, 2017, Schleswig-Holstein’s state parliament voted against ratifying these, with North-Rhine Westphalia and Hesse since announcing their intention to follow suit. Without full state support, the intended changes did not take effect, further delaying reform. A Federal Administrative Court ruling on 26 October, 2017 upheld the ban on online casinos and poker. The ruling, which is now the subject of a constitutional complaint, appears to have led to action by local regulators seeking to enforce the prohibition of online casinos by issuing interdiction letters to operators. Paymentblocking initiatives are also being pursued.

Operator type: All licences are available to private operators save for lottery, which is reserved exclusively for the monopoly provider, Camelot.

Status: Any operator that transacts with, or advertises to, British

residents requires a licence from the Gambling Commission. Licensed operators are required to source gambling software from commissionlicensed businesses. The UK government has announced its intention to increase Remote Gaming Duty at the next budget to cover a shortfall in lost tax revenue resulting from a reduction in maximum stakes on fixed odds betting terminals from £100 to £2.

GREECE

Regulated gambling products: Sports betting, horse race betting and lottery.

Operator type: All products are exclusively reserved for the monopoly providers, although 24 transitional licences for private operators remain active, with all products permitted.

Status: The enabling regulations that implement a Greek online gambling licensing regime are yet to be implemented. In 2012, a ‘transition period’ commenced, whereby the Greek government granted 24 transitional licences to operators, enabling them to keep transacting with Greek residents. In September 2018, the Government published draft amendments to the country’s Gambling Law which if implemented as proposed, introduce an open licensing regime with unlimited licences, prohibit RNG-based games and maintain the current 35% GGR tax.

Operator type: Only the state monopolies (Szerencsejáték Zrt. and Magyar Lóversenyfogadást-Szervezo Kft) and local concession companies can apply for a licence.

Status: Amendments to Hungarian gambling law came into force on 1 October, 2015 and allow only two land-based casinos to hold remote casino concessions. The regulator has since issued fines, a number of which have been challenged, against unlicensed operators that continue to target the market. In June 2017, the ECJ determined Hungary’s gambling regime to be incompatible with Article 56 TFEU. A subsequent ECJ decision in February 2018 ruled against the Hungarian requirement that online gambling operators must have a land-based licence to offer online gambling services to Hungarian citizens, further strengthening arguments that the current regime is incompatible with EU law. The Hungarian Ministry of Justice has stated its intention to continue to seek to enforce the existing regime despite the most recent ruling. A draft bill that would introduce payment-blocking measures was notified to the EC on 15 December, 2017, although the bill does not yet appear to have been adopted.

IRELAND

Regulated gambling products: Online gaming is not specifically accounted for in Ireland’s outdated legislation and as such is currently unregulated.

Operator type: Online betting regulated since August 2015.

Status: Ireland is currently updating its legislation, which will create a comprehensive igaming regime. In January 2018, the Irish Cabinet gave the go-ahead to draft a new version of a bill that was first proposed in 2013. This has now been subsumed into the Gambling Control Bill 2018, which was introduced by Ireland’s opposition party in February 2018 as a private member’s bill. Amendments to the Gaming and Lotteries Act 1956 have also been proposed. Legislative progress is not expected until late 2018 at the earliest. The Irish government has announced its 2019 budget, doubling the betting duty from 1% to 2% tax on turnover with effect from 1 January, 2019.

Status: The Stability Law 2016, passed in December 2015, introduces various measures affecting the remote gambling industry, including tax changes and a tender process for the award of 120 new online gaming licences. The tender process for applications closed on 19 March, 2018. On 7 August, 2018, the Italian parliament approved a decree which prohibits gambling advertising and sponsorship. The ban took effect on 14 July, 2018, although ongoing advertising contracts remain valid until the earlier of their expiration date or 14 July, 2019. The sponsorship ban will apply from 1 January, 2019.

LUXEMBOURG

Regulated gambling products: Lottery.

Operator type: Monopoly.

Status: The general prohibition on gambling appears sufficiently wide to cover all forms of online gambling.

Operator type: Private operators can apply for a local licence (except for lottery products).

Status: Malta has approved a new Gaming Act that replaces all existing gaming legislation with a single piece of legislation, supplemented by secondary legislation. The Gaming Act, together with directives and regulations, is effective as of 1 August, 2018.

Status: The Dutch parliament’s lower house approved the Remote Gambling Bill in 2016, which will introduce an online gambling licensing regime. In September 2018, the Government opened a public consultation on the implementing regulations of the Remote Gambling Bill, which will be followed by debate and a vote in the Senate, expected in early 2019. It is understood that operators that have previously been fined by the Dutch regulator will not be eligible for a licence. In the interim, the regulator continues to implement enforcement measures against operators targeting Dutch players, having imposed recent sanctions against three well-known operators.

NORWAY

Regulated gambling products: Sports betting, horse race betting and lottery.

Operator type: Online gambling is reserved for the two monopoly providers, Norsk Tipping and Norsk Rikstoto.

Status: The monopoly has extended its offering to include live betting, online bingo and casino games in an attempt to redirect traffic from unlicensed sites. The Norwegian regulator continues to step up enforcement efforts against unregulated operators, local banks and payment service providers. On 4 June, 2018, the Ministry of Culture notified a draft regulation to the European Commission that would establish payment-blocking measures. The standstill period ended on 5 September, 2018. The European Gaming and Betting Association is understood to have filed a legal challenge against the proposed measures.

Operator type: Betting licences are available for companies with a representative in Poland. Casino and poker are reserved for a state monopoly.

Status: Legislation enacted 1 January, 2012 permits betting. Online gaming (including poker) is no longer prohibited as of 1 April, 2017, although the exclusive rights to offer such products are reserved for a state monopoly. Provisions that provide for the establishment of a blacklist of unlicensed operators and ISP and payment blocking came into force on 1 July, 2017. The blacklist contains more than 1,000 domain names.

Operator type: Any EU/EEA operator can apply to be granted a licence for online gambling. Lottery games and land-based fixedodds sports betting remain reserved for a monopoly.

Status: A regulated market since 2015. Although operators can now apply for licences, their Portuguese revenue streams are subject to comparatively high tax rates, particularly in sports betting (8-16% tax on turnover). In 2015, the RGA filed a state-aid case with the EC challenging the Portuguese betting tax as breaking EU trade rules. On 13 October, 2018, the government approved the state budget law for 2019 which proposes the introduction of a flat rate of 25% tax on GGY for all games. The final version is expected to be approved at the end of November 2018.

Operator type: Any operator from an EU/EEA jurisdiction or the Swiss Confederation can apply for a licence. Lottery games remain reserved for the monopoly.

Status: The Romanian government passed legislation in 2014 that allows entities within the EU to apply for a licence, imposes a reform on licence fees and eliminates many (but not all) of the tax burdens placed on player revenues. The Gambling Law (as amended) introduced a legal framework for a fully regulated online gambling market and requires licences to be held by online gambling operators, as well as software providers, payment processors, affiliates and testing labs. After some delay, the secondary legislation that fully implemented the new licensing regime came into force on 26 February, 2016.

Operator type: Monopoly, save that land-based sports-betting operators can offer services online owing to a legal loophole.

Status: In November 2016, a bill amending the existing gambling legal framework was approved. The amendments, which entered into force on 1 January, 2017, included the introduction of ISP and payment blocking of illegal online gambling offerings in the Slovak territory. Slovakia’s Financial Directorate began to perform its supervisory function over these blocking measures from 1 July, 2017. New draft legislation has been notified to the EC with a view to liberalising the market in 2019. The proposed legislation, if passed, will allow private EU/EEA operators to apply for online gambling licences.

Operator type: Online gambling must be operated by land-based casinos or lotteries and, as a result, only the monopoly holds online licences in Slovenia.

Status: Draft amendments to the Gaming Act were published in 2015, which aim to remove the current local establishment requirement. The proposal is yet to be submitted to the Slovenian parliament, although it is expected to be adopted in 2018. Whether any amendments will introduce a formal licensing system remains unclear.

Operator type: Private operators can apply for licences for all gambling products save for lottery.

Status: First online licences were issued on 1 June, 2012. Operators must hold a general licence and a specific licence, both issued by the National Gambling Commission, for each activity. The Spanish regulatory body DGOJ has formally opened its third call for tender, with applications for online licences accepted from operators for a period of one year, until 18 December, 2018. On 16 January, 2018, online poker liquidity sharing between Spain and France came into effect. The 2018 parliamentary budget was passed into law in June 2018, resulting in a reduction to gambling tax effective as of 1 July, 2018.

Operator type: Only public-benefit organisations, the horse racing industry and the state lottery may obtain a licence. No licences are available for private operators, although this will change with the introduction of the new legal framework.

Status: The Swedish parliament adopted a bill that will introduce an online-gambling licensing regime.The law is expected to enter into force on 1 January, 2019, with the licence application process open as of 1 August, 2018.

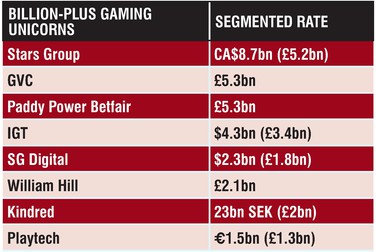

In the post-dotcom era, a handful of technology companies have risen to the mythical status of unicorn ($1bn+ valuation), or even super unicorn ($100bn+). The huge publicity surrounding these companies, which include the likes of Alphabet and Amazon, makes it tempting to see the rise of unicorns as a growing trend. But that’s not necessarily the case. In fact, as the fairytale-inspired name first coined by the venture capitalist Aileen Lee suggests, they are still exceedingly rare, with only 0.07% of start-ups ever reaching such rarefied status.

This is especially true in the gaming industry, where only a handful of companies have ever been able to claim multi-billion-dollar valuations. And in almost all cases, they are publicly listed operators that have only broken the billion-dollar benchmark through one or more significant key acquisitions (see Figure 1).

Consolidation among the big players in the sector has accelerated in recent years, with mega deals materialising principally for the following reasons:

• an emphasis on squeezing out the competition;

• expansion into new territories via large-scale mergers;

• land grabs in regulated markets; and

• forward-thinking regulatory opportunities in emerging (and soon to be regulated) markets.

These drivers have seen Paddy Power Betfair, GVC and the Stars Group all successfully execute multi-billion-dollar deals to consolidate dominant market positions and play on a more global scale, particularly with the sportsbook-led opening of the US.

European markets, according to Thompson Reuters Intelligence research, have seen a resurgence in cross-sector mega deals, with the value of M&A activity doubling year-on-year in the year to date. Interestingly, though, the number of transactions has fallen by 18% to 6,201, the lowest level since 2005. So fewer companies have been buying, but when they have they’ve been digging deep.

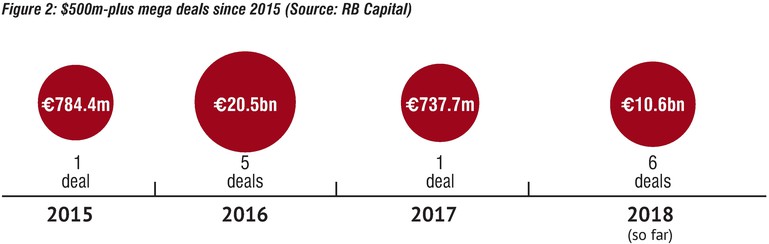

The same can’t be said for gaming. RB Capital’s M&A Monitor data has highlighted a fluctuation in €500m-plus mega deals (see table), with €32.6bn spent in the last four years, a flurry of five huge acquisitions materialising every 24 months, and a minor downward trend in deal size from 2015 to the present day.

Both 2016 and 2018 have seen the largest splurges with €20.5bn spent on deals two years ago, including the two mammoth mergers of Ladbrokes-Coral and Paddy Power-Betfair, while 2018 so far (total spend of €10.6bn) has had a distinctly new market feel about it.

This year has seen Paddy Power once again active in acquiring US fantasy sports brand FanDuel, the Stars Group splashing out €4bn to purchase Skybet and serial accumulator GVC coming back for more following its 2017 Bwin acquisition by snapping up the recently merged Ladbrokes Coral business.

Some commentators have suggested blockbuster transactions have had their day, with the most significant deals already done and those businesses now predicted to pursue more organic growth strategies. But there are many reasons why further M&A action is on the cards.

Just the beginning

The number of mega transactions may have fluctuated in recent times but there is still huge value to be found across an array of growing assets.

Five years or so ago, most deals in the UK and Europe were driven by a mission to boost or establish scale or rapidly gain first-mover market share in regulated or soon-to-be regulated markets. However, most 2018 deals have been steered by the promise, and now growing reality, of US state-by-state regulation.

Although it is early days for other states to jump on the bandwagon, investor appetite from US operators and European suppliers has been intense. And with ‘real’ revenues now coming through Nevada ($247m in wagers in August), New Jersey ($100m) and even Delaware ($17m), this is only set to continue. Remember this has all happened during the traditionally quiet period ahead of the busiest months for sportsbooks of October and November, when all four major US sports’ biggest events coincide.

Crucially, there has been a shift in the structure of recent transactions and we have seen a spike in interest from private equity and venture capital firms as several states open for business and others look to follow suit.

Sportradar and Genius Sports have both been the focus of VC/PE investment that aims to capitalise on US market expansion. Interestingly, both companies offer data services, which savvy investment firms know will always be in demand, and thus offer stable and consistent annuity revenue unaffected by high customer acquisition costs, taxes and/or levies. They will also be invaluable when aiming to engage and retain existing players and acquire and attract a new, younger, mobile-first audience.

These are far from small deals. Indeed, the Canada Pension Plan Investment Board has teamed up with growth equity firm TCV to part with more than $700m in exchange for a 39% stake in Sportradar. Meanwhile, renowned PE investor Apax Partners, which has previous gaming experience investing in, and since exiting, Candy Crush developer King, went one step further. It swallowed up sports data and media rights distributor Genius Sports Group with the capital injection allowing it to pursue its international expansion strategy, largely in the US.

We expect these types of structured deals to continue, especially around data-driven software suppliers and fast-growing platform providers, with exit valuations that will tempt even the most risk averse PE/VC firm given their medium- and long-term outlook.

The potential of a larger-scale re-regulated US gaming and betting market is finally turning heads, then. But while attention has been focused on cross-Atlantic activity in recent months, we shouldn’t neglect European M&A. It is worth remembering that the everchanging nature of markets here, alongside several other factors, is likely to encourage further M&A and potentially far more mega deals than in the US.

The first driver of this lies in the pressures created in dot-country markets and by increasing regulation across Europe. We are seeing these in regulated markets (including the overly saturated and increasingly volatile UK), maturing regulated markets such as Italy and Spain and recently regulated markets in developing regions such as Eastern Europe.

In the UK, several operators are managing increasingly severe financial regulatory fines for repeated marketing abuses. Next year will also see the UK and various licensed jurisdictions, among them Gibraltar, Alderney and the Isle of Man, confront an unclear and worryingly uncertain future outside the European Union.

These pressures may drive stakeholders to sell or divest certain assets, while intensifying competition in other mature territories will continue to push an increasing number of smaller brands and suppliers to speed dial the right sell-side brokerage.

In maturing regulated markets such as Italy, where reputable brands are still working out how to market products under a draconian advertising ban, and Spain, which was initially hard to operate in but is now showing promise following a change in the tax regime, participants will see M&A as a medium-term option to either get out for good or remain and push for increasing market share.

Lastly, in newly regulated and regulating markets including Romania, Czech Republic, Bulgaria, Poland and others, expect a return to the good old land-grab days. There, experienced deal makers such as GVC are already making incursions into markets such as Georgia with an eye to the future and educated, mobile and tech-savvy audiences.

Other operators are sure to follow GVC’s lead into these markets, but with many of the transformative transactions in the sector having now completed, it will become harder for other gaming companies to join them among the ranks of the unicorns.

In summary, over the next 18-24 months expect ever more creative acquisitions stateside as buyer risk starts to fall in the face of medium-term gains.

On this side of the pond we anticipate a flurry of short-term UKbased activity with players exiting while they’re (pre-Brexit) ahead.

Medium-term M&A is expected to be strong for central and southern Europe. And the Nordics will (as always) be at the mercy of longer-term pension fund trackers. The M&A market will remain flush with activity for a good time to come. So watch this space.

Ben Robinson is co-founder of boutique advisory firm RB Capital, focused on the igaming, fintech and media sectors. RB Capital works with both start-ups and scale-ups looking to raise capital and also established companies looking to take their business to the next level or initiate a liquidity event.